Shifting away from using diesel in construction & development

Hands up all those who think COP26 feels like years ago, rather than just four months ago? Whilst the conference can be described at best as a ‘qualified success’, a striking element of its outcome was the sheer number of 30 to 40 year targets for decarbonisation, with little focus on the immediate work needed to limit climate change.

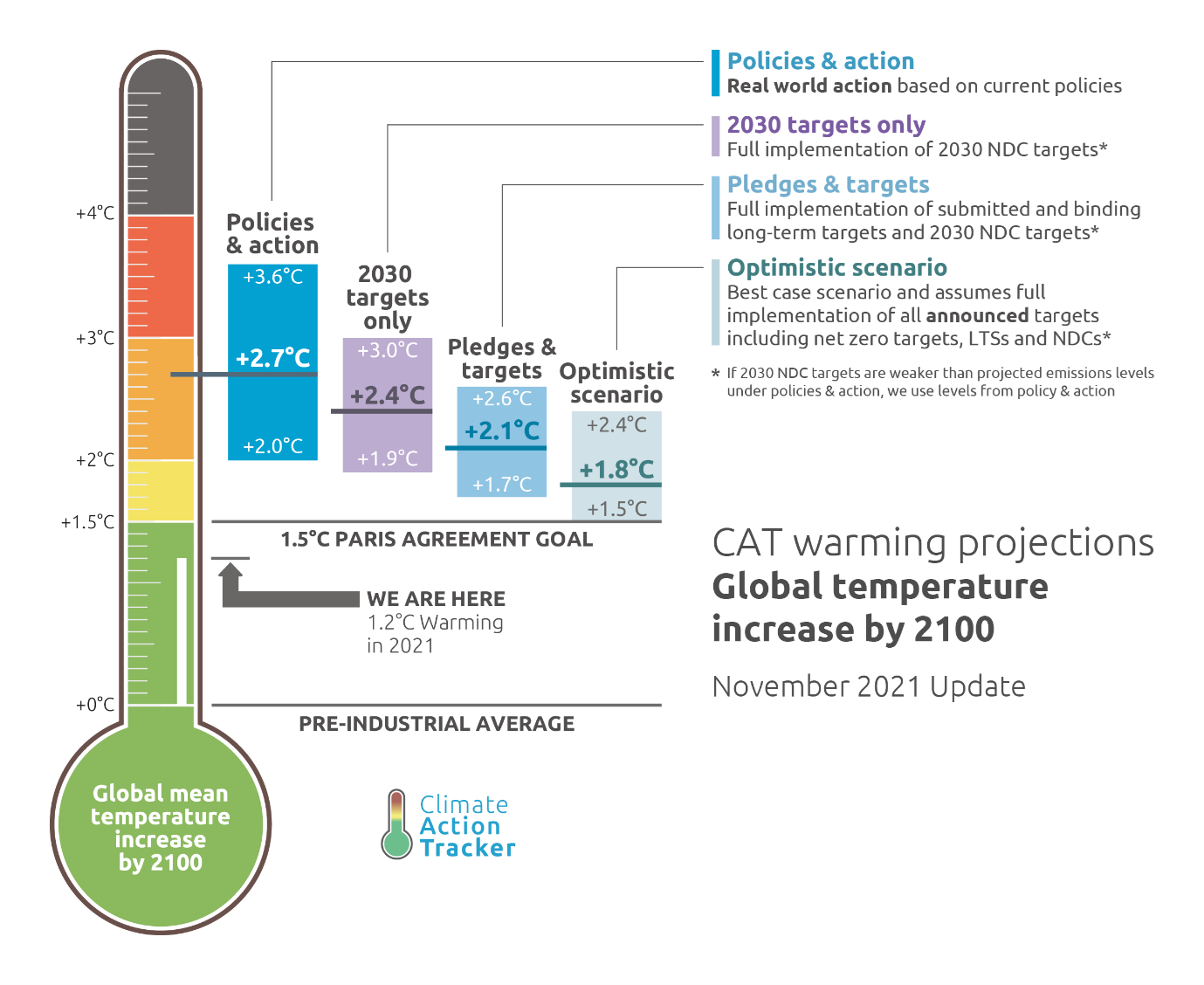

Optimistic and pessimistic global warming projections to 2100

This is quite incredible given we are already 1.2 degrees Celsius above the pre-industrial average temperature, with even optimistic projections suggesting a lower range of 1.5 degrees Celsius by 2100 – enough to force significant transitions in land and ecosystems, energy sources, urban and infrastructure development, and industrial systems. The IPCC expertly covers what a 1.5 degree change could mean here – yet the situation is predicted to be far worse if projections are solely based on planned near-term action.

How Countries compare in setting their Net-Zero Strategies (2022)

In fairness to the UK Government, its publication of a formal Net Zero Strategy in November 2021 places it ahead of a number of other developed economies – despite its spending commitments and initial primary legislative programme being somewhat modest versus those of countries such as Germany and Canada (more on that later). Its strategy includes:

• Its decarbonisation pathways to net zero by 2050, including illustrative scenarios;

• Policies and proposals to reduce emissions for each sector; and

• Cross-cutting action to support the transition, including a number of near-term actions.

Its sectoral analysis and focus for action includes construction – an essential element, given the industry currently accounts for circa 38% of global energy related emissions, many of which are produced by diesel-driven equipment. Page 128 of the hefty 368 page document reflects the importance of reducing emissions from what it describes as ‘Industrial non-road mobile machinery’ (NRMM):

“NRMM covers a wide variety of machinery across the economy (e.g. diggers, combine harvesters, generators, cranes), with total emissions of around 12 MtCO2 e per year. Industrial NRMM accounts for around 6 MtCO2 e coming from construction, mining, and manufacturing, with the remaining emissions largely attributed to agriculture, and some to buildings and transport.

New technologies have begun to penetrate markets for some NRMM uses, for example electrification technologies, particularly for small, light duty equipment. Government intervention is likely to be necessary to ensure low carbon technologies continue to be developed and ensure uptake at the level needed to reach carbon budgets and net zero.” (our emphasis)

Part of this approach will naturally need to include fuel switching – the industry powering its equipment using lower carbon fuels to reduce emissions and ultimately weaning itself off the use of diesel. As this article explores, the starting pistol has already been fired by Government for this change – but is the industry ready?

A MAJOR POLICY SHIFT: ELIMINATING THE USE OF RED DIESEL IN THE CONSTRUCTION INDUSTRY

‘Red Diesel’ has been used by the construction and development industry for decades in powering operations and machinery to bring forward development. Red diesel is diesel which contains red dye and other chemical markers to indicate that it is rebated diesel and has therefore been subject to less fuel duty than normal (white) road fuel diesel. The red marker allows HM Revenue and Customs (HMRC) to check whether red diesel is being used illegally.

Red diesel attracts significantly less fuel duty than white diesel with duty of 46.81 pence per litre less for red diesel than white diesel. Red diesel is also subject to a reduced 5% rate of VAT for supplies up to 2,300 litres. Industry has therefore been incentivised to use this fuel in its non-road operations – a situation clearly at odds with the urgent need to decarbonise to limit global warming.

This situation was referred to by Chancellor of the Exchequer Rishi Sunak as “a £2.4bn tax break for pollution that’s also hindered the development of cleaner alternatives” in making his announcement in his 2020 budget statement that red diesel could no longer be used in construction (amongst other industries). This demand became legislative through the Finance Bill (2021) and subsequent secondary legislation – restricting the entitlement to use red diesel and rebated biofuels from April 2022 to a limited number of qualifying purposes, including agriculture. You can read the basis of the Government’s legislative changes, and what it means for industry, here.

At the time, this measure looked catalytic as a series of major construction or development companies began to explicitly promote their greener credentials. This included:

• Costain planning to be net zero carbon by 2035 at the latest;

• British Land aiming to be net zero carbon by 2030; and

• Mace announcing that it had achieved net zero-carbon status in 2020, whilst announcing a 2026 business strategy that included helping their clients reduce their carbon footprint and scope 3 Greenhouse Gas emissions.

So far so good. But what of the technology available today to enable companies to move beyond the humble diesel generator in powering on-site operations and machinery, if they aren’t prepared to pay full price for commercial diesel? This is where two important factors come into play – what plant hire companies offer or plan to offer; and the will & financial muscle of the constructor or developer to pay and use alternatives.

Example of Sunbelt’s greener fleet

Sunbelt Rentals, a leading provider of plant and machinery across the world, have already made extensive preparations for the switch as shown here. This includes the development of a ‘green range’ that encompasses two types of alternative technology and fuel:

• Electric plant and vehicles, including excavators and dumpers; and

• A range of HVO Fuel powered generators as a lower carbon power source, as shown in the infographic below. ‘HVO’ stands for Hydrotreated Vegetable Oil and is a type of biodiesel. HVO is often referred to as renewable diesel, and can be used as a direct replacement for diesel in existing generators – although, as Sunbelt have shown, newer generators will significantly reduce emissions.

Sunbelt’s route to reduced emissions (2022)

HVO fuel providers claim a number of environmental benefits in its equivalent use vs. diesel. Aggreko, another leading hire company, claims that “HVO drop-in fuel gives you the power to cut harmful NOx emissions by up to 25% without cutting your generator’s performance”. When twinned with a latest stage generator, it has also been claimed to reduce carbon emissions by up to 90% versus standard diesel.

HVO is an extremely useful fuel, albeit a transition one. What about genuine net-zero power options? Whilst these are not immediately available for hire today, leading construction companies are taking the plunge and trialling them direct to provide early industry reference points to show their feasibility in practice. Zero-emission hydrogen power provider AFC Energy plc, through their ebullient Chief Commercial Officer Mark Bailey, announced a tie-up this week with Keltbray for the latter to trial a hydrogen powered fuel cell system to replace a diesel generator on a UK construction site at the end of Quarter 2 this year, whilst also promoting the results to plant hire companies.

The key benefit of AFC Energy’s fuel cell systems versus those of HVO-powered generators is that they can genuinely be called ‘zero-emission’, with the only by-product of its power generation being demineralised water. The key challenge for this, and other similar technologies today, is proving a track record for reliability and ease of use where it counts on the ground – and we’d expect others to follow Keltbray’s lead in trialling net-zero products in the short-term.

So, a number of transitional technologies exist and the potential for genuine net-zero technologies exist. But does the will to make a wholesale move to these products really exist? Recent evidence on the back of significant diesel price rises suggests otherwise…..

RECENT PRICE INFLATION CAUSES MAJOR HEADACHES FOR THE INDUSTRY

A double whammy of cost inflation has hit the construction and development industry over recent weeks. The first is a significant rise in inflation from historically low levels, caused in part by rocketing gas prices – leading to significant material and labour cost increases across all parts of the supply chain. Russia’s invasion of Ukraine, and the fall out of resulting sanctions, has exacerbated these increases via Brent Crude hitting an eye watering $125 a barrel in early March.

Brent Crude Pricing, March 2021 to March 2022 (Taken 15 March 2022)

To paraphrase the late great Denis Healey, this has ‘squeezed the pips’ of the industry ahead of the red diesel ban, leading to a number of calls for it to either be delayed or be permanently kicked into the long grass:

“The measure is going to cripple the construction industry.” (Welsh Civil Engineering & Groundworks business)

“We have seen electric plant technology coming out, but it isn’t viable yet. It’s not versatile enough for us to use it in every situation where we need it. If we were working on a field at an architectural dig, there is nowhere to charge it up.” (Director of another contracting firm)

“These are unprecedented times and after rejecting industry pleas on minimal exemptions for plant vehicles that could not be electrified, such as mobile cranes, this policy change arrives in the middle of a perfect storm on British energy costs and so a twelve-month deferral on removing the red diesel rebate is pragmatic.” (Richard Beresford, Chief Executive of the National Federation of Builders)

You can read more on the squeeze that construction firms face here.

This leaves a real short-term dilemma. As a minimum, firms will be forced to pass on cost increases up the chain simply to survive, further ramping up inflationary pressures on the economy. In challenging times, it is also highly unlikely that the majority of companies will have the bandwidth or wherewithal to make major equipment or fuel switching changes in short order. Should the Government therefore change course?

WHAT SHOULD GOVERNMENT AND INDUSTRY DO NEXT?

Our view that the Government should continue on the same course to ban red diesel for most uses on the 1st of April – but it must be far more ambitious in its spending to accelerate the availability of viable new technology to be used on sites. If the Government is genuinely serious about leading from the front in creating a ‘green industrial revolution’, it really has no alternative to this plan.

Let’s look at those relevant spending plans. In 2021 it announced a £40m ‘Red Diesel Replacement Competition’, alongside a £55m Industrial Fuel Switching competition to support the development of lower carbon power technologies to be accelerated. It then announced a further fund, the hydrogen accelerator programme, in early 2022 – details of which can be found here.

These are all good starts as funds and focus on the right things, but there are two obvious flaws with them. Firstly, the funding is extremely modest in scale. Compare the UK’s funding with Germany’s 1.4bn Euro investment in Hydrogen and Fuel Cell technologies alone over the next ten years. Can it really claim to be leading the way in promoting a green industrial revolution given this paucity?

Secondly, creating lots of individually assessed funding streams – as seen writ large in regeneration funding over the past twenty years – often acts as a barrier for SMEs and challenger businesses with great ideas and concepts to access accelerator funding. This tends to shift the balance towards large companies, often in consortia, to hoover the funding given their ability to dedicate time and resource to access it. We therefore strongly advocate bringing together these programmes into a single pot for net-zero technologies and having a number of funding rounds in any year to keep up with technological innovation. Why not call it the Green Industrial Revolution Fund and (frankly) open it up to allcomers to accelerate growth?

In the meantime, we have significant sympathy with those in the construction industry that are wrestling with some extremely difficult decisions over the next few months to keep development going. Coming back to the introductory graphs to this article however, there is no time to lose in accelerating the deployment of lower or zero-carbon technologies in building new homes, commercial spaces or infrastructure – and this imperative trumps all others.